Sticker price: -$978 a decade

Instead, make $1,600 in a decade.

Should a checking account cost anything? In my opinion, hell no. And in an ideal world, not only should a checking account not be something you pay for, a checking account should pay you.

According to the LATimes, only 28% of checking accounts are free & the average monthly maintenance fees are about $13 costing about $150 a year. According to a

Also, according to a NerdWallet study, the average cost of checking accounts in a decade is $978 and for the more than 109 million U.S. households that have checking accounts, the total average annual cost of the accounts is about $10.7 billion. Moreover, they add, “if those households switched to one of the most consumer-friendly checking accounts, they’d save $7.3 billion altogether in just one year.”

WOW.

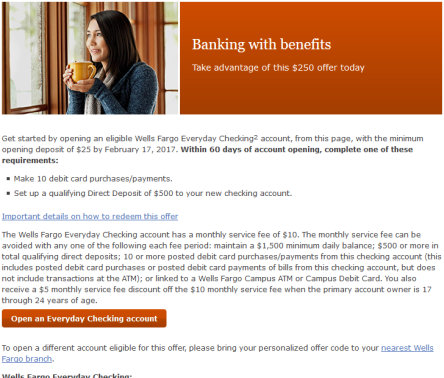

Earlier today, I opened a Wells Fargo checking account. With a sign-up bonus, I was paid $255. Technically I won’t see that money for a couple of months, but it’s worth it anyway. Free money is free money! I’m adding it to my suite of awesome checking accounts [see my list of 5] which I will never pay a penny for.

Basically, I found out about this $250 offer through thepennyhoarder.com (one of my favorite personal finance sites) and it was too good to turn down. On the downside, to keep it free I have to either have direct deposit (my income is too inconsistent to depend on that) or make 10 debit card payments. That latter one is easy because I found out that I could do one of two easy things which take no more than a few minutes each 1) pay my MetroCard in 25¢ increments 4x in one shot 2) pay my health insurance with a minimum of at least $1 (I haven’t tried smaller amounts) 10x in one shot.

Doesn’t this lovely photo of someone having a warm drink looking out into the cold outside just make you want to earn money from home? No? Well, at least one of your problems wouldn’t be worrying about paying a corrupt bank when you just want to put your money somewhere! Ahem, more on my bank philosophies another time.

I don’t know how long I’ll keep up that 10x monthly payment habit or if I’ll get a job I want to set up direct deposit for. If I don’t want it anymore, I could definitely live without it. I’ll cancel it and recycle my card and all the damn paper they’ve sent me. It wouldn’t be the first time I did all that. Last year, I opened a Capital One checking account just to be paid $25. Not too shabby for 20 minutes of work. Two years ago, I think I did the same thing for TD bank. In college, it was Chase. Opened, got paid, canceled. The only downside is that I wouldn’t be able to take advantage of any new member bonuses they have for the same banks.

On average, I’ve earned $150 in bonuses/interest per year plus all I save from the headaches and fees of many popular accounts. In a decade, I’d say I would make about $1,500 – and I get to invest that hundred-ish I would have spent elsewhere bringing my “price” to an extra $1,600 in my pocket, er, checking account, just for not using all those overpriced accounts.

I could also live without all those checking accounts because I have this ideal combo (no ATM fees internationally, free checks, 1% interest, a physical branch close to home, access to my balance/transactions via text, referral bonuses, and values which align with my financial independence goals) of checking accounts which I’ve almost perfected…

- Charles Schwab*: I remember this “Investor Checking” account being a bit confusing to open because you have to link it to a brokerage account (which I have $1 in), but I knew one thing which is that I never have to pay an ATM fee again… anywhere in the world. Plus I got more checks than I’d ever need. This is my main account and I haven’t paid anything to maintain it.

- Ally: Technically, it’s not a checking but, with a combo of the Money Market Account and Online Savings, I have a debit card and interest of 1%. Yeah, I can only access it 6x a month but having that to put an emergency fund is pretty convenient. There is also $10 available for reimbursement if you’re not using a connected ATM… which there are many of.

- Capital One 360: For a few years, I didn’t want to bank with a branch for of all the fees and minimums, but I found out that this account not online had no minimum but also had the benefit of having cash deposit options… like Wells Fargo will also have once that’s all set up. Ally and Charles Schwab don’t have options to run up to an ATM and deposit cash, but with Capital One 360, I do. Also, when I opened it, they gave me $25 and if you use my link, you’ll get that too. Lastly, when I was without a bank branch, I would “deposit” cash by giving it to someone I trust then asking them to write me a check which I would use an app to deposit or have them send me money through my Cash account.

- Rush Card: Does a prepaid card qualify as a checking account? Not sure, but, well I got about $26 from just opening it, have a no-fee ATM near my house at a Sterling bank, and have a card. It took some time to fund it via my PayPal, but free money is free money. I’m not sure how long I’ll keep it, but if I use it just once every 90 days, there are no fees. I don’t think I would want to give any money to them either. It’s led by Russell Simmons and as an org, there was an incident in Oct ’15 that they were sued for and I haven’t heard great things about their customer service. They’re coming out with more of a rewards program though sooo, I may just stick around.

- Digit: I’m also not sure if this qualifies as a “checking” either. I suppose it doesn’t because it just holds money like PayPal, Cash, etc. but one thing I love about this “auto-saving” account is that it has an awesome mission (worth quoting, “We’re finance hackers that see the overwhelming pile of crap that exists in the world of consumer finance and have taken up arms to improve the status quo through better software and better customer experiences; which will lead in our calculations to a financially healthier population.” Besides their values, my favorite part about Digit is the ability to text them when I want to know my balance and recent transactions.

Two other checking accounts I have which are worth noting:

- Aspiration: Great values like Digit, but the interest isn’t as high as Ally’s, actually the interest is more than Charles Schwab and there are no international ATM fees… hmm I might switch out my Schwab for Aspiration now that I think about it. I’ll let you know!

- Bank of Internet: I’m still setting this one up, but there’s a way to get 1.25% interest without a minimum sooo I’m figuring that out.

So what about your checking accounts? Have you ever had to pay for any services or are you “paid” for having them? Was this a helpful post? As always, let me know your thoughts in the comments, please.

PS NerdWallet has an awesome search tool to find a checking account combo that works well for you which filters from your zip code, average balance, and monthly direct deposit. Check it out!

*These links are not personal affiliate links except for Capital One and Digit…and I don’t have access to my Cash app code so I just used my sister’s =)

Written on January 27, 2017

Updated on February 4, 2017